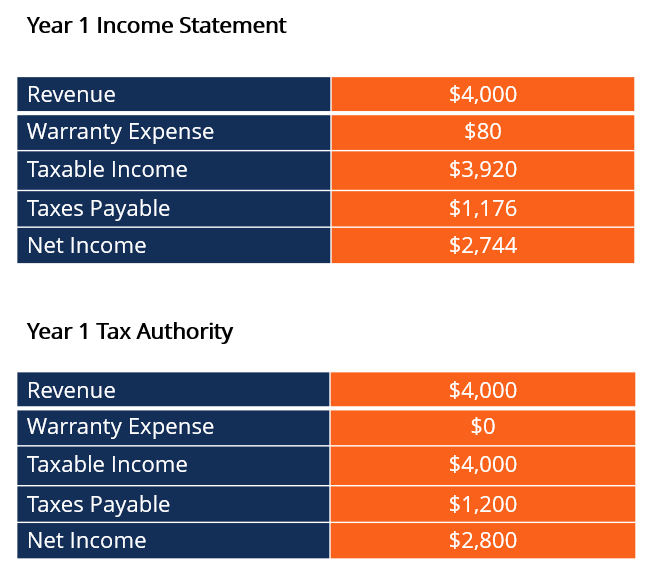

Balancing Charge Deferred Tax. when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary differences between book (ifrs, gaap) tax and. as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. There are two categories of temporary differences: (1) taxable temporary differences that will. this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance.

from corporatefinanceinstitute.com

a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary differences between book (ifrs, gaap) tax and. when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. (1) taxable temporary differences that will. as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance. There are two categories of temporary differences: this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to.

Deferred Tax Liability (or Asset) How It's Created in Accounting

Balancing Charge Deferred Tax this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary differences between book (ifrs, gaap) tax and. this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance. under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. There are two categories of temporary differences: (1) taxable temporary differences that will. when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to.